:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/AFRFRYFICJA7FLRHUCVRWRTU3A.png)

Willy Woo is an entrepreneur, angel investor, derivatives trader and cryptocurrency enthusiast.

In this guest feature, Woo takes aim at the prevailing notion that China's bitcoin markets account for 98% of trading, suggesting that the real number is closer to 80%.

Today, China's exchanges report 98% of global volume, a figure that would suggest a huge dominance by its markets.

Unfortunately, we know that most of this volume is fake.

Unlike the rest of the world, China-based exchanges are unique in that they do not charge fees on bitcoin trades. Instead they make money via withdrawal charges out of the exchange. Further, these fees reduce as your trading volume increases, so this incentivizes traders to bolster this figure by buying and selling from themselves at zero cost.

Still, there's a ocean of data coming from the markets, and they hold hidden secrets.

In this study, I'll peer into the data and attempt (as far as I know) the first estimate of true China-based volumes using data driven methods.

Starting points

For this post, I'll define "true volume" as what the volumes would have been, had the exchanges charged a trading fee.

Prior estimates (really just educated guesses) have put Chinese volumes at 50% of the global market. Let's see how well this compares with the data.

To begin, we must remember that China was not always a zero-fee market.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/LL2HABQ5WNFQZIWN37GR6VXAPM.png)

BTCC, the first China-based exchange, started with 0.3% fees on trades. Likewise the second Chinese exchange, OKCoin, initially charged 0.3%.

Then, on 24th September 2013, BTCC instigated what was to be a three-month experiment in zero fees. This started an arms race between all the domestic exchanges, heralding in an era of zero fees from which China has never returned.

But, how do we know the effect this had on volumes?

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/CRJDGU63AVEBFEIAOC3GMVDK2A.png)

For one, there was an immediate spike. Expressed as a ratio to non-Chinese volume, it went from 17% to well over 100% in barely six weeks.

This visualization is useful in one other aspect.

We can see China's exchange volume growth was steadily increasing at a predictable rate (of about 4% week on week) before the introduction of zero fees.

This becomes our first tool to estimate true volume, as we can use this steady growth to extrapolate what volumes may have been like had this trend continued.

'Legit volumes'

Now, there is one market in China where the volumes have never been faked, LocalBitcoins, a decentralized marketplace where buyers and sellers connect and trade.

Here’s what its volumes look like:

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/7PHAE4EDR5BXZI3EDCKPMN562A.png)

was founded in June 2012, and you can see it gained traction rapidly. By Q4 2013, we can see it began tracking global on-exchange volumes quite well.

The exchange is also available in many countries globally, meaning each market has a ratio between “on the streets” volume and what volume their local online exchange is doing.

This ratio differs depending on local conditions, but the two will track each over over time.

This will be our second tool in our estimation strategy.

We can use LocalBitcoin's volume to show local market demand, and scale it up to estimate exchange volumes.

Putting it together

We are now ready to reconstruct real Chinese exchange volume.

The historical estimates has three phases:

- Real Chinese volume before the zero fees era

- Chinese volumes were in a predictable growth pattern prior to the zero fees era, so we can extrapolate the growth for long enough to get us to the next phase

- Once LocalBitcoins entered the picture, and was given enough time for it to gain adoption, we can scale up its volumes to estimate what the exchanges should have been doing as the two are tightly correlated.

The final composite looks like this:

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/LB6PCD5J25FZ5PS6RUBCPGF6NQ.png)

From this composite, we can reconstruct the true global market volume.

Here's the estimated true volume vs the reported volume. The differences are significant:

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/ZY63ZLKNZJCWXIF2CTZDE4J6ZY.png)

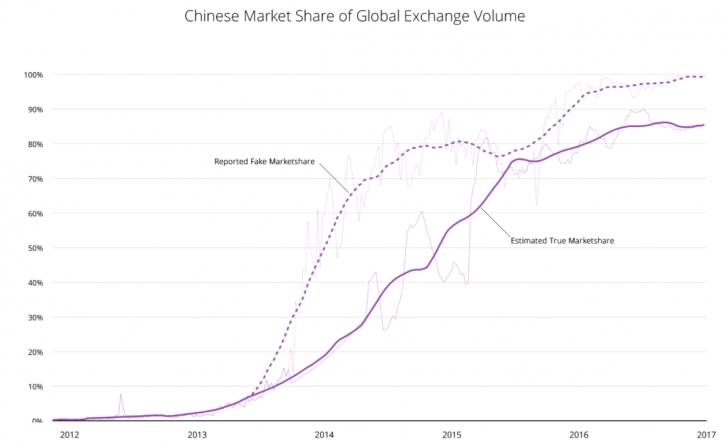

Expressed as Chinese marketshare of global exchange volume, it looks like this:

Expressed as a ratio of fake volumes to true volumes, it looks like this:

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/DS2LGXMU6BCNXIAWSKLMVWMJIQ.png)

Yes, it's been almost 40x overreported at times.

Still dominant

Previous educated guesses have put the real marketshare at 50%, but the data implies it's much higher, around 85%.

China is still the dominant players controlling bitcoin volume, but not nearly as dominant as reported volumes suggest, about 10-40x less dominant, depending on the week.

Data from CoinDesk Research, for example, based on publicly available data, indicates the reported figure to be 95%.

It's also worth mentioning that exchange volume doesn't make up as much of global bitcoin trade as one might assume.

The exchanges may set the prices, but most of the volume happens off exchanges in over-the-counter trades, so true globally traded volume is (supposedly) hidden.

Using similar methods to these here, I can probably make an estimate of OTC trade, but I'll leave that to another day.

Visit Woo's blog to read more cryptocurrency markets coverage.

False teeth image via Shutterstock

:format(webp)/downloads.coindesk.com/arc/failsafe/user/1x1.png)