The Media's Cringeworthy Coverage of Bitcoin's Latest Price Surge

From April Fools jokes to "mystery" orders fueling bitcoin's recent rally, mainstream media still struggles to get basic aspects of the crypto market.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/DF5XJX4UJ5APTFB2KWBLI3JAE4.jpg)

/arc-photo-coindesk/arc2-prod/public/LXF2COBSKBCNHNRE3WTK2BZ7GE.png)

UPDATE (9, April 00:09 UTC): Oliver von Landsberg-Sadie, CEO of BCB Group was given a right of reply to defend his statements regarding his findings as cited by Reuters.

---------

Mainstream news coverage of cryptocurrency is often disingenuous or factually incorrect – that’s certainly no surprise given the nascent technology is widely misunderstood.

But if one would have thought that recent milestones – bitcoin’s 10th anniversary, the arrival of crypto projects from the likes of JP Morgan and Facebook – would have encouraged the media to get smarter, this week’s news shows attitudes at major publishers haven’t changed much.

This is especially true during times of heavy market activity like that of bitcoin’s April 2 breakout, which saw its price rise 17 percent over a 30-minute period.

, the move was foreshadowed by changes in market data and sentiment. With volatility hitting multi-year lows, multiple technical indicators flashings signs of a bottom and fundamental catalysts (the upcoming halving) combining, there were plenty of developments that signaled a change might be on its way.

Still, far from examining developments (or asking serious questions), much of the mainstream media’s coverage devolved into outright theory and speculation.

Here’s the worst of what was a genuinely bad bunch.

Gizmodo

While articles like these from Gizmodo are useful in gauging retail sentiment – ie, determining where the average Joe sits in terms of understanding and valuing cryptocurrency – they, unfortunately aren’t useful for anyone who wants to be informed.

Writers like Matt Novak have a point – novice retail investors were given a bitter taste in 2018, when the market for cryptocurrencies took a turn for the worse. Still, that’s no excuse for not educating yourself or your readers, who, without such learning, may repeat mistakes.

The article reads:

Without spending too much time on this statement, there are a few incorrect passages, that in particular, don’t ring true. For one, bitcoin definitely can act as a medium of exchange. It can be, and today is used to facilitate the commerce and trade of goods between parties, a core fundamental function of modern money.

Next, it’s backed by the computer operators that mine the network itself, all of whom invest real dollars, manpower and equipment in ensuring the network is functional.

Finally, while the cost of mining bitcoin remains high thanks to its large energy consumption, this does not mean it cannot run off renewable energy and take advantage of natural events that reduce the cost and lessen the impact to the environment.

It seems mainstream media tends to forget that the cost of mining bitcoin’s physical competitor, gold, is perhaps even more guilty of harming the earth's environment as its miners regularly tear apart massive landscapes and leave behind loads of toxic waste.

To state that this will forever be bitcoin’s final form borders on ignorance as well, as we have seen time and time again that the evolution of technologies usually comes from a solution to fix a specific problem.

Reuters

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/KU4SXFCQUJHQJADZS3OAWWJYFM.png)

One of the least offensive of the bunch, a Reuter’s report that cited a solo “mystery” buy order as the main cause for a huge price spike still offered a confused take by focusing in on a sole market irregularity.

In particular, it highlights a claim made by the chief executive of cryptocurrency firm BCB Group, Oliver von Landsberg-Sadie, who argued the case that the move was the responsibility of a single buyer.

The article reads:

This is hard to corroborate with independent analysis as the article did not provide evidence of the orders, merely statements that negate other factors.

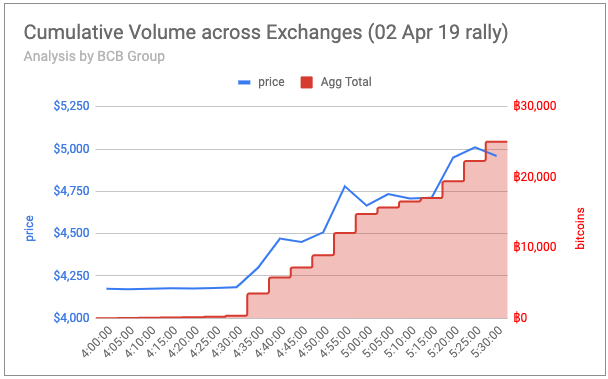

As the price climbed higher, this resulted in a snowball effect of buying as shorts were closed and limit buy orders were triggered, causing its price to rise faster and higher.

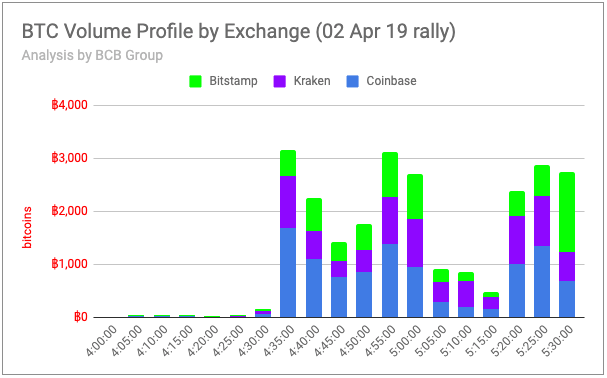

Using an hourly view of bitcoin’s price we can see just how much volume was recorded during a single trading period by looking at the volume bars and order books and then noting their readings. At 4:00 UTC on April 2, Coinbase recorded a total of 6,889 units in a single hour and Bitstamp handled close to 3,798 units while Kraken had the least at 4,121 bitcoin units traded in the same hour.

This created a total of 14,808 units traded in the hour of the surge, yet Reuters and CNBC claimed 7,000 units were purchased on each of the three different exchanges in tandem by a single entity at the time of the surge.

Needless to say at the time the numbers didn't quite add up.

Also of note, data shows that growing buy volume began to increase substantially across most major exchanges, not just the three highlighted in the article.

However, Oliver reached out to Coindesk in order to support his claim by providing the following:

BCB Group agrees with CoinDesk’s findings for the 4am-5am period, but this window captures just half of the purchase volume and half the price rally.

If we shift the observation window back 30 minutes and look at the 4:30am-5:30am period, we see the full action.

The purchase order was initiated by 3 simultaneous purchases of 10 BTC on each of these exchanges at exactly 4:33am.

Over the next hour, a total of 24,853 BTC changed hands in a highly uniform and synchronous pattern, quite far outside of the normal hourly trading volume of roughly $1-2m per hour on these three exchanges. Kraken traded 7545 BTC, Bitstamp traded 6739 BTC and Coinbase traded 10,420 BTC.

Then there is the “Fast Money,” notorious amongst the crypto trading community for getting things so wrong they act as a counter-indicator.

Indeed, a mere 38 seconds into this CNBC Fast Money video an analyst makes a comment regarding bitcoin’s movement above the 200-daily moving average occurring for the first time since May when in fact it was March 2018, leaving room for speculation about what else they could be misleading.

Throughout 2018, CNBC and its subsequent panel show Fast Money made some outrageous comments regarding the direction of bitcoin’s price and advice to investors.

Comments such as “don’t fear the dip, bitcoin will more than double in 2018” and “what will hit 25k first, bitcoin or the DOW,” it’s no wonder they have claimed such a bad reputation for calling a correct directional bias and sticking to it.

The word “overstated” comes to mind when you look at the numbers – that would imply the market capitalization of all cryptocurrencies could increase nearly $40 billion on that back of a harmless prank, and that an entire body of global traders would price in such an event.

The market for crypto may be small... but that small? We doubt it.

Disclosure: The author holds no cryptocurrency at time of writing.

Newspapers image via Shutterstock

:format(webp)/downloads.coindesk.com/arc/failsafe/user/1x1.png)