As Bitcoin Bounces Back Above $7K, Popular Analysts Say Monthly Close Is Pivotal

Bitcoin needs to rise by more than $1,000 in the next three days to invalidate bearish pressures, according to Mike Novogratz and Willy Woo.

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/coindesk/SUCRDCJHVBBOHLN7PYEIV27BGY.jpg)

/arc-photo-coindesk/arc2-prod/public/LXF2COBSKBCNHNRE3WTK2BZ7GE.png)

Bitcoin has charted a relief rally in the last 24 hours, yet it still needs to rise by more than $1,000 in the next three days to invalidate bearish pressures, according to prominent analysts.

The recovery from six-month lows around $6,500 had been expected, with key indicators reporting extreme oversold conditions and intraday charts flashing signs of seller exhaustion.

While the bounce is encouraging, a bullish reversal is likely still a way off.

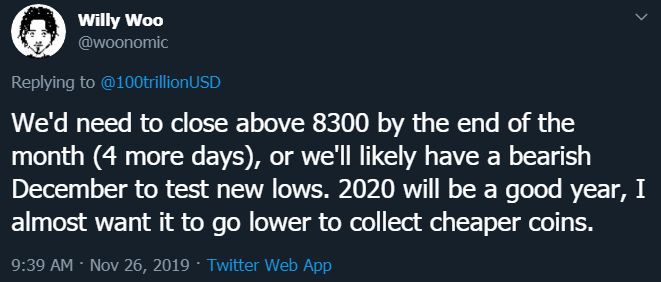

"Bitcoin needs to close above $8,300 by the end of the month or we'll likely have a bearish December to test new lows," popular market analyst and Adaptive Fund partner, Willy Woo, tweeted during the Asian trading hours.

The top cryptocurrency is currently changing hands at $7,200 on Bitstamp, representing a 10.5 percent rise from the six-month low of $6,515 registered on Monday.

Essentially, bitcoin needs to rally more than 15 percent and print a UTC close above $8,300 on Nov. 30, or a bearish engulfing candle will be created on the monthly chart.

A bearish engulfing pattern consists of a green candlestick, representing a price gain, followed by a large down (black or red) candlestick that eclipses or "engulfs" the previous candle, as seen in the chart below.

On the monthly scale, BTC opened at $8,300 on Oct. 1 and closed at $9,150 on Oct. 31, forming a green candle. The follow-through has been dismal this month. Prices opened at $9,158 on Nov. 1 and are currently trading near $7,200.

Essentially, November's price drop has engulfed the October candle's body – the spread between open and close.

The bearish setup will be confirmed if bitcoin ends November below $8,300 (October's opening price). That would imply a resumption of the sell-off from the June high of $13,880 and could invite stronger selling pressure, possibly yielding a deeper drop below $6,000.

That said, bearish engulfing patterns have trapped sellers in the past, according to Woo. So, sellers should observe caution even if the bearish pattern is confirmed – more so, as BTC has already dropped by more than 50 percent in the last five months and could recover some ground ahead of the miners reward halving, due in May 2020.

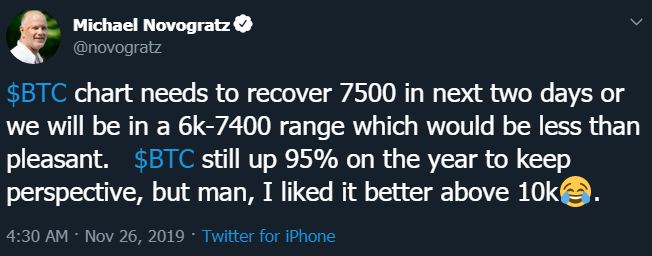

While Woo is citing $8,300 as the level to beat for the bulls, Michael Novogratz, the billionaire CEO of Galaxy Digital, feels bitcoin needs to break above $7,500 to avoid being stuck in the less pleasant $6,000–$7,400 range.

A move above $7,500 in the next couple of days could be seen and may yield rise to $8,000. The outlook, however, will remain bearish as long as the cryptocurrency is trapped in a five-month falling trendline seen below.

Weekly chart

A weekly close (Sunday, UTC) above the upper edge of the falling channel, currently at $8,990, is needed to confirm a bullish breakout, which, if confirmed, would mean a resumption of the bull market from lows near $4,100 seen in early April.

Realistically, bitcoin is more likely to form a bearish engulfing candle, as prices usually consolidate near lows for some time after a notable sell-off. This is because investor confidence tanks during a bear market and takes time to recover.

All-in-all, the crypto is likely to trade in the range of $7,500 to $6,500 over the next few days. Any gains above the descending 10-day moving average, currently at $7,628, will likely be short-lived.

:format(webp)/downloads.coindesk.com/arc/failsafe/user/1x1.png)